We are entering the hot months. Compared to February through June or September through November of any given year in any type of market, you will see fewer sellers and fewer buyers.

And it makes sense, right? So many people are escaping the heat by leaving town, cooling off in pools that are barely cold anymore, or hiding inside their dark homes with the AC on and cold drinks in their hands.

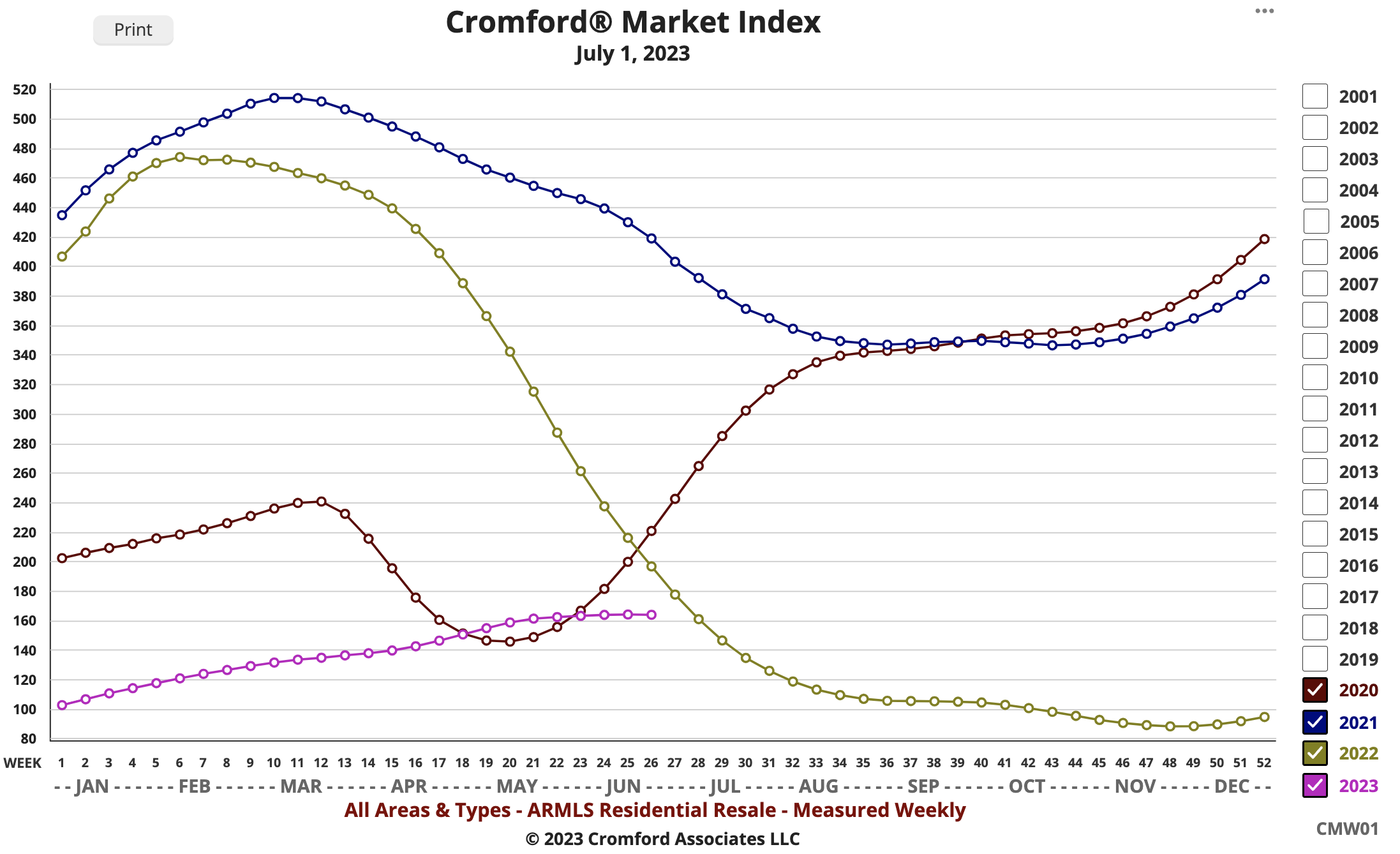

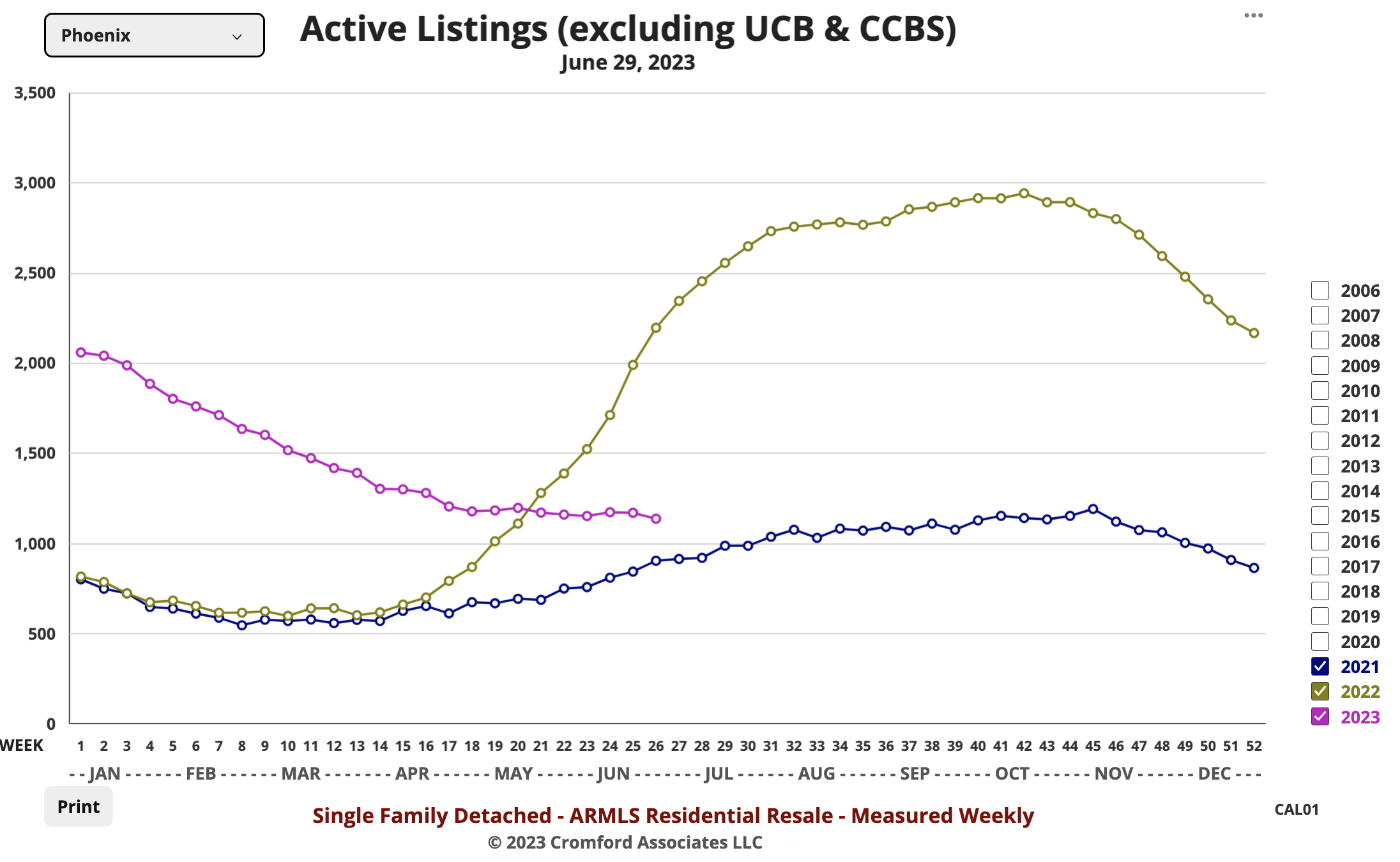

So, as the Cromford Report folks look back at the first six months, we are still seeing fewer listings than last year and prices that are pretty much the same.

In our experienced opinions, you might want to brave the heat to find a deal over the summer, rather than waiting until more people come back as the nights begin to cool in October.

“Here are the basics – the ARMLS numbers for July 1, 2023 compared with July 1, 2022 for all areas & types:

- Active Listings (excluding UCB & CCBS): 11,545 versus 14,406 last year – down 20% – and down 1.6% from 11,730 last month

- Active Listings (including UCB & CCBS): 14,406 versus 17,261 last year – down 16% – and down 4.4% compared with 15,062 last month

- Monthly Sales: 7,377 versus 8,113 last year – down 9.1% – and down 9.0% from 8,110 last month

- Monthly Average Sales Price per Sq. Ft.: $287.76 versus $300.43 last year – down 4.2% – but up 1.5% from $283.71 last month

Comparisons with this time last year are getting easier, as a year ago the market was deteriorating as demand from institutional investors and iBuyers collapsed. A steep rise in interest rates had spooked the market and ordinary buyers were holding their breath too.

A year later we have a market which is seeing very low demand and even lower supply. With the 30 year fixed interest rate stuck around 7%, most homeowners do not want to sell and buyers are struggling to qualify and afford a home. Buyers are unimpressed with the low inventory of re-sale homes and are increasingly turning to new built homes. Developers are enjoying strong orders, firmer prices and healthy margins, but have relatively low inventory of homes for sale and a weak pipeline of new permits to build. The strongest sector in the housing market is single-family new construction.

Some people drastically overstate the importance of interest rates in determining home prices. Interest rates are important but when they move higher they lower supply as well as demand. It is the balance between supply and demand that determines how prices move. At the moment supply is much weaker than demand so prices are increasing, as they have since January.

For homeowners, rising prices are reassuring, but for agents, the low volume is a huge problem. There are remarkably few new listings and closings are declining as we enter the summer doldrums. Title companies, lenders, warranty providers, inspectors and appraisers are all suffering from a prolonged weakness in transaction volume. While interest rates remain at 6.75% or higher, we appear unlikely to see much improvement. In fact rising prices will make it even harder for buyers to close on a home. However if interest rates were to fall to 6% or below, we could see a sharp increase in demand and an improvement in supply too.

We will shortly see the average $/SF for closings overtake the figure from a year ago. At the moment the gap is 4.2%, but last year’s prices were falling fast and this year we are seeing a rise of almost 3% in just 2 months. The third quarter is notorious for weakness in average pricing, but even if closed prices stay flat for the next 3 months, annual appreciation will have turned positive by the end of the quarter.”

So, what’s the take-away from all of this? Inventory is not great, but prices continue to climb and will climb further at the end of the summer.

If you are a buyer, get out there now. If you are a seller, start preparing your property over the summer to list in September.