We’ve been checking in more regularly on the market, of course. This market watch is supporting what Michael Ore of the Cromford Report was predicting, as reported in our last regular market update.

Here are some highlights of that:

The valley housing market has changed much less than you might expect.

While there have been some negative trends, sales prices are still rising and the affects have been lesser than other economic sectors.

Comparing April 1 of this year to April 1 of last year:

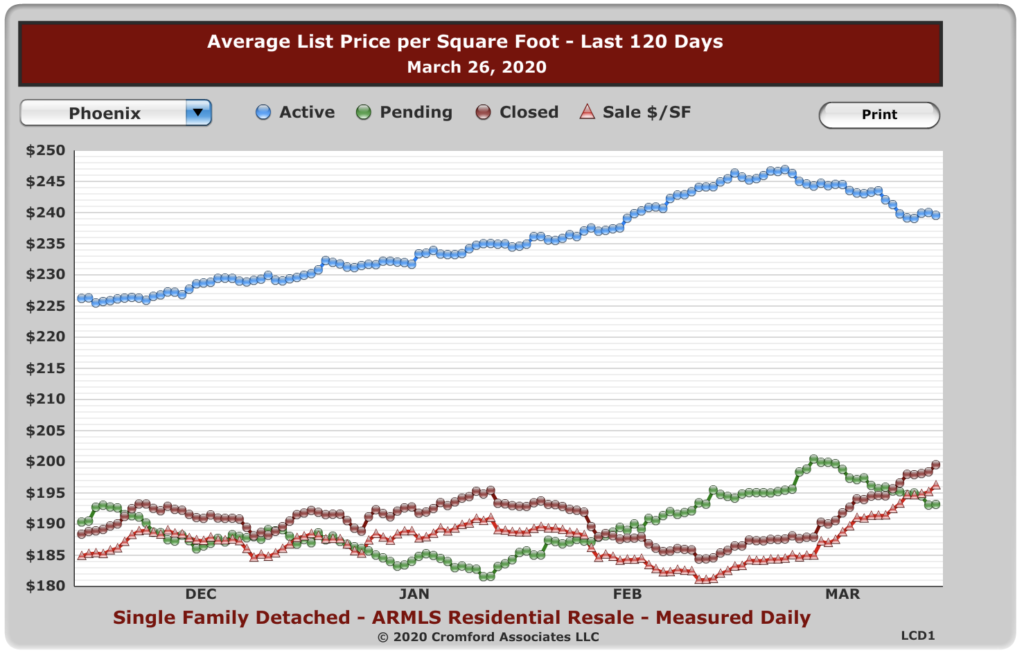

Active Listings (excluding UCB & CCBS): 13,211 versus 18,650 last year – down 29.2% – but up 20.1% from 11,003 last month

Under Contract Listings (including Pending, CCBS & UCB): 10,152 versus 11,707 last year – down 13.3% – and down 15.3% from 11,988 last month

Monthly Sales: 8,840 versus 8,489 last year – up 4.1% – and up 18.2% from 7,476 last month

Monthly Average Sales Price per Sq. Ft.: $186.47 versus $172.01 last year – up 8.4% – and up 0.8% from $184.94 last month

In summary, supply went up, demand came down, sales remained strong and prices went up.

So, look at this market watch chart. It is showing that list prices are coming down over the last few weeks, which makes sense. People are worried. But the key here is that sales prices are still going up.

If that does not speak to what is going on in the market, I don’t know what does. There is still scarcity and people still need homes.

At the very least, predictions that the real estate market will crash like the stock market are simply not turning out to be true.

As the days tick down before your Close of Escrow (COE), you are going to focus on a couple things: the final walk-through and reviewing your settlement statement for your closing meeting.

Walk Through. Get it? Oh, we crack ourselves up.

The purpose of the final walk-through is to make certain that the property is in the same condition for close as it was when you made an offer.

If the seller is doing repairs, then we need to make certain they were completed. We can hold up the close if they were not.

We will do a final walk-through together and we will look for these things.

This is also a good time to call the utility companies and move them over to your name. Don’t forget this! It is a pain in the hind quarters to have to sit around waiting for the natural gas guy “anywhere in a window between 9:15 am and 7:45 pm” because you forgot to call ahead to simply switch the name on the account.

Assuming the final walk-through looks good, we will review the settlement statement with you.

A settlement statement an accounting by the title and escrow company of who owes whom what. So, for instance the seller is credited for the price of the home and you are debited for that price (via a loan, of course).

You are credited for the earnest money that you sent in at the beginning of the process. You may be credited for seller-paid closing costs, if there were any.

You will also see:

Loan origination charges (what you pay your lender to get started)

Any other lender fees that may exist.

The down payment

Payments in to the escrow account, to get you started paying for taxes and insurance every year.

If you are buying in to an HOA, you will see fees for that and up-front dues.

At the bottom of the settlement statement will be the amount you will bring to closing. Unlike the earnest money check, this check must be a cashier’s check, or you can wire it a day or two before.

So, to wrap it all up, you meet at the title company. One of us is almost always there to answer questions.

Get ready to sign two tall stacks of documents: one for title and one for your loan. Expect between one and one and a half hours to complete it all.

With all of that complete, the title company will send notice to the county recorder’s office to let them know that you now own the property. Once we get confirmation back from them that recordation has occurred, we can meet you at the property to give you the keys.

Simple!

Now, get ready to do it in real life.

If you have any questions, please call us at 602-456-9388.

We are almost there, Trust me! In this installment, we want you to know the three main contingencies that would allow you to leave a contract and get your earnest money back.

The Three Contingencies remind me of the Three Sisters, or the three agricultural staples of north America, winter squash, maize and beans.

Yep. I’m a gardener. Can you tell?

But, the three contingencies are also healthy and work together to protect you, the buyer.

The Inspection Contingency is very broad, to the surprise of many. Basically, if you don’t like almost anything you find wrong and if you report it in the first 10 days of the inspection period, you can exit the contract and get your earnest money back.

We typically tell folks that they should think beyond just plumbing and electrical. Take the time to knock on neighbors’ doors and ask them what they think of the street. Drive by on a Friday night and crack the window to see if the neighborhood gets loud –this is important if you live downtown and in the age of AirBnB.

At the end your inspections, will will present to the seller a list of items you want fixed, or a notice that you are leaving the contract.

Two things to note. First, if you don’t respond in the 10 days, it is the same as saying you approve of the sale going ahead. Second, if you respond on day 5, you don’t get to report anything you find after that. You missed your chance.

The Loan Contingency basically allows you to leave the contract if your lender decides that you can’t get a loan for some reason.

However, if you wait until you are just about to close on the house and the lender finds out that, for instance, you did not report your debt and income properly, then you could lose your earnest money.

It’s another reason why you need to make sure you disclose all of the important debt and income information to your mortgage broker right up front.

The Appraisal Contingency allows you to get out of the loan if the home does not appraise for the sales price. Basically, your lender wants to know what they think the house is worth. They don’t care what you agreed to with the seller.

If the appraisal comes in “above value,” it just means that the appraiser thinks the house is worth more than you are paying for it. Congrats.

If the appraisal comes in below value, then one of four things has to happen:

The seller drops the price to the appraised value

The buyer makes up the difference in cash.

The seller and buyer meet somewhere in the middle.

You walk away from the deal.

In a seller’s market, don’t expect the seller to drop the price much, if at all.

We are glad you’ve made it this far. You are the few, the elite. Get ready for the inspection period!

Yep, this series may seem a little long in the age of Twitter. But reading this will save you so much time and heartache.

Plus, after years in the business, we know that some of our clients prefer to read things like this, then have us walk through a slide show. We are here for you, fellow introverts!

In this installment, we will cover the all-important inspection period.

The most important thing to know about the inspection is that you can back out for any reason, as long as you do it in the 10 days. If you are uncomfortable with the inspection, or the seller refuses to fix what you ask, do what you gotta do!

We use these guys the most, but you have the right to shop around!

If you talk to the neighbors and they tell you something that alarms you, you can pull out.

This part is not just about pipes and plumbing. But, if you find something after the 10-day period, or after you send your inspection report to the seller, then you are out of luck.

So, do a full inspection. This included a termite inspection.

As the old joke goes, “there are two types of homes in Arizona. Those that have had termites and those that will.” Don’t be afraid if you find evidence of termites. Be concerned if the seller has not remedied the situtation.

Another thing to keep in mind is that the inspection is just a general inspection. The job of the inspector is to look over things and tell you what he or she sees that could be wrong. If the inspector writes a note about the A/C not blowing enough cold air, for instance, you may want to have a specialist in right away to have a look.

Once you’ve had the inspection, the inspector will show you through the report at the property, and will point out all of the things that he or she finds.

Note: You will find things wrong with every home, especially older homes! Your decision will be just how important those things are to you.

We the consult with you about what you want to ask the seller to fix –all, some or none. We put that in a Buyer Inspection Notice and Seller Response form, or a “BINSR”, and we will present it to the seller.

If the seller refuses to fix some or all of the things, you have a right to back out of the contract and get your earnest money back. (More on that later.)

The appraisal is the second big thing that we are working on at this point in the process. It may not happen during the inspection period, but it can.

The appraisal is just you lender deciding what they think the house is worth. They won’t lend you more money than that.

The appraiser will come by the house to have a look and give an estimate of value.

Like the inspection, if the appraisal does not come in at asking price, you have a right to exit the contract and get your earnest money back.

I remember when I bought my first house being introduced to a title and escrow company. I understood that they process paperwork, but I nobody gave me any context as to why.

In this installment, we will help you understand the most important points of the title and escrow process.

Ensure that the person selling the house has the right (through a title on the home) to sell it to you. This is the “title” part of the name.

Track all of the money and paperwork so that there is transparency and certainty about who gets what at the end of the process. This is the “escrow” part of the name.

The escrow period begins when there is an agreement on the contract, or a “meeting of the minds.” It ends when the parties either cancel the contract (we will cover that later) or the escrow closes –as in a complete sale.

The first thing you will see happen is that a courier will come to pick up an earnest money deposit from you. This is a deposit, held by the title and escrow company, which shows that you are serious. If you back out of the contract for reasons not outlined in the contract, you can lose that money. It usually is about 1% of the total contract price. So, $3,000 for a $300,000 contract. You will get this back at the end, unless you breech the contract.

This check can be a personal check.

So, on to the concept of title and escrow, generally. You know when you buy a car, you get a copy of the title. Simple right? Well, with an auto title, the name of the current owner is written right there on the title. If they owe money on the car, that is noted.

The real estate, the same basic thing happens. However, because houses are around for so long and represent so much more money, somebody really needs to do a “title search” to make certain that nobody is going to come to your door in a year and tell you that the person who sold you the house never had the right to do that.

Seems crazy, but this stuff happens. Otherwise, we would not have these systems in place. Heck after the Great Recession, there were many properties with “clouds” on the title, meaning there was some question as to who owned it in the past. Perhaps a short sale or foreclosure clouded the title.

Anyway, unlike with auto titles, the title companies will offer insurance, of sorts. The seller pays for title insurance so that if anybody challenges the title, the title company will back you up with their lawyers, etc.

So, it is incumbent on the title company to do a good title search.

In that process, and within 5 days after the beginning of the escrow period, the title company will issue a title report. This is their report, which describes the property, previous ownership and will confirm that the current owner has the right to sell you the property.

Read it! Please!

If there is any place in this process where you could find something odd, this is one of them. If the city put an easement on the property, it will show here. If the is some question about the lot lines between this and the next property, you will see it here.

The “escrow” part of their work at this point entails holding on to your earnest money deposit, tracking the terms of the contract and preparing for you to take title in a way that you want, i.e., “Jane and John Doe, enjoying joint tenancy.”

They will have more to do at the close of escrow, and we will cover that later.

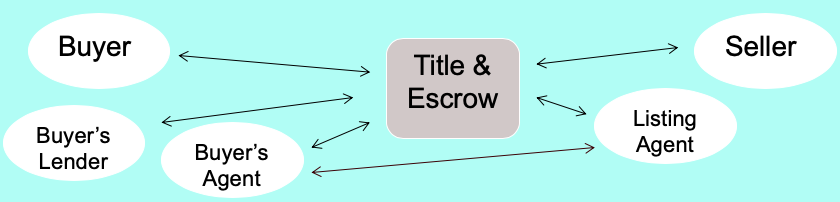

Finally, just so you know the players on the field and how we interact. We, the buyer’s agent will coordinate with you, your lender and the title company. We will also negotiate with the listing agent on your behalf.

That way, you don’t need to speak with the seller. All of the negotiation is done for you, at your direction.

You have the right to choose your title company. We may still have to negotiate with the seller to get them to use that company. While we can’t force you to use any particular company, we have had the best luck with Old Republic Title.

When we meet a new client, especially a first time home buyer, we grab a cup of coffee and preview the home buying and sales contract process and.

Nobody explained the process for me when I bought my first house and I paid for it. It makes a huge difference to know what to expect next in the process; what to be ready for.

You deserve better, and we deliver.

So, it’s high time that I put the home buying process in writing so you can read about it in the comfort of your home, in your jammies with a cup of your favorite beverage.

So, you found the house you want and you are ready to go.

Hold on. We want to make certain you are not paying too much.

The first thing we do is run comps to make certain they are not asking above market price. Your biggest concern is that you don’t pay too much.

You also don’t want to pay $500 for an appraisal, just to find out that the house is over-priced and the seller is not willing to negotiate.

The second thing we do is go over all of the sales contract with you. We can do that in person, or over the phone; with all of us reviewing the documents on our computers.

We will explain the sales contract as slowly or as quickly as slowly as you would like to understand all of the terms.

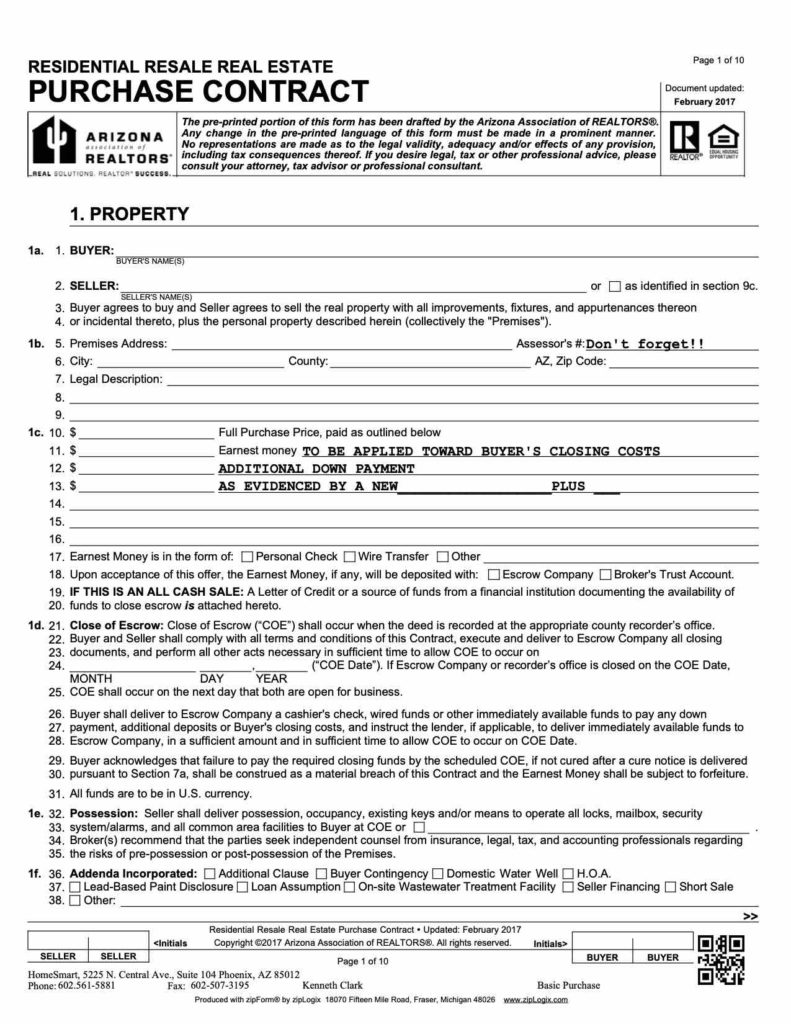

You can expect to see some or all of these sales contracts and addendums:

The 9-page sales contract.

The lead-based paint addendum, if the home was built prior to 1978.

A home owner’s association addendum, which tell the HOA what information to disclose to you.

A seller property disclosure addendum (“SPDS”), in which the seller should disclose all they know about the property.

A wire fraud advisory, which just tells you that you should be careful of wire fraud.

An affiliated business disclosure, in which our broker just discloses that they have sister businesses, such as title services or home warranty services, and that you are not required to use them. We don’t, by the way.

If both sides of the contract are represented by our broker (even if we’ve never met the other agent), there is a consent to limited dual representation.

So, plan for about an hour to go over all of these and ask questions about what is coming next.

We often use digital signing tools these days, such as Docusign or others so that you can sign from the comfort of your office, or in your PJs at home.

Once we submit the contract, you can expect to see either:

A counter offer from the seller,

A rejection from the seller or,

An acceptance from the seller.

We do all of the negotiating for you. So, you can relax and cheer us on.

Sometimes, but not often, the counter offer process goes back and forth for a few rounds, but that seldom lasts more than a day.

So, be available for calls and consultation.

With contract acceptance, we are off to the next stage: the escrow period.

When we meet a new client, especially a first time home buyer, we grab a cup of coffee and preview the home buying process.

Nobody explained the process for me when I bought my first house and I paid for it. It makes a huge difference to know what to expect next in the process; what to be ready for.

You deserve better, and we deliver.

So, it’s high time that I put the home buying process in writing so you can read about it in the comfort of your home, in your jammies with a cup of your favorite beverage.

A few big, on-line home search companies have made a lot of money giving you inaccurate information.

Those same companies have really high-priced lawyers, so I won’t mention their names.

But I can tell you the most important thing: their business model is not built around getting you the most accurate information. It is built around selling ad space to realtors like us.

We don’t buy that ad space, by the way.

So, for instance, if a certain zip code does not have enough active listings on their site, they sometimes show pending listings as active listings in order to get more eyeballs on their site, so they can sell more ad space to us.

That is a huge waste of time and sometimes an emotional drain for you, the buyer. You get excited about a property, call up your agent and ask “why am I not seeing this on the portal you created for me?” Typically, it’s because it is no longer active, yet you see it on that other site.

Here’s the other thing to know: 99% of the data originates from our MLS system, and is just repeated out on their sites –just with less useful information and more bling.

We, as agents, must update changes to our listings within 48 hours, or we can be reprimanded in some way. That can cost us money.

All of those changes go to the other sites.

So, why not get the accurate information, direct from the source?

Thus, the MLS portal.

After we meet you and create a formal relationship, we will create a portal for you. We are not the type of agents who just create a portal and say, “tell me what you want to look at.” That’s lazy.

First, we would prefer to show you around the MLS system, as there are useful tools on there, which you will not find on the other sites. Second, because we have so many years of experience in the market, we like to look for new listings every day.

That way, we can weed out the ones that may not be a good fit, even if they look great on line, or vise versa. We know the neighborhoods, we hear the gossip and we can either advise you to stay away from something or suggest how an area might work better for you.

Context is crucial, is what we are saying.

Once we have used the power of the portal to narrow down your best 5 or 6 options, we will go out and see the properties in person. If none of those work for you, we go to the next, or watch for daily updates.

We make it a policy not to see more than 6 properties in one tour. You may be a house-hunting machine. But I guarantee that after the first 5 properties, they all start to blend together in your memory –even if you are taking notes.

We find that cramming in too many homes is not the best process for decision making.