The Oh My Ears (OME) New Music Festival is an annual event where we invite unique and adventurous ensembles, solo artists, and projects to perform works by modern composers.

The OME Festival has historically featured its performers in an eclectic variety of venues, from traditional concert halls to art galleries, bars, and cafes.

This year they will be at Phoenix College and Cibo’s Carriage House. OME is proud to be a presenter of new music in Phoenix for 10 years.

It says a lot about what it takes to sell an all-cash co-op, versus a traditional home, which you can purchase with a loan. Co-op properties stay on the market for much longer, as you are waiting for a buyer to come with all cash. Whereas our new listing in the Garfield neighborhood, was listed on Saturday and we have an accepted offer now, chosen from multiple offers.

It’s a shame, because co-op properties are often meticulously-maintained and offer a very stable alternative, especially if you travel a lot.

The price of our listing in midtown has come down a bit and the sellers are very reasonable, though not in a rush. So, have a look.

520 W. Clarendon Ave, Unit G2. $284,000, 2br/1.75 ba, 1,320sf. There are a few pristine co-op apartments still in central and downtown Phoenix. Most were built in the 1960s and only a few maintain that mid-century charm. This is one of them. But, on top of that, the owners of this unit opened up the kitchen since and completely remodeled since they purchased the home in 2021. This home is being sold with all of the unique furniture, as an option for the buyer. This secure community is just steps from dining, light rail and shopping. You can lounge in the pool or chill in the historic commons knowing that your investment is being maintained and cared for as a co-op uniquely is. See the listing and more photos here.

1423 E McKinley St. Listed at $339,000, 2br/1ba, 686sf. This property has the beauty of a historic bungalow and the money saving features that you will appreciate for years. The buyer can apply for the historic district property tax reduction AND the property is already zoned for two residences. With a large back yard, RV gate and full RV hookup, there is plenty of room to grow. The covered patio in the back houses an outdoor kitchen, a super efficient heat pump water heater, an RO water system and laundry. The property saves huge amounts of water with low flow fixtures, a front-loading washer, low water-use plants and a grey water system that feeds trees. Not to mention the PV solar system, extra attic insulation, high efficiency HVAC, remote thermostat, insulated floor, double pane windows and recently-remodeled kitchen with induction range.

I think that, while we are not in recovery mode, we are starting to see the outlines of it on the horizon. Active listings are coming up, and hopefully that will slow price growth a little going forward. For now, though, listings under contract are not as high as we’d like them to be.

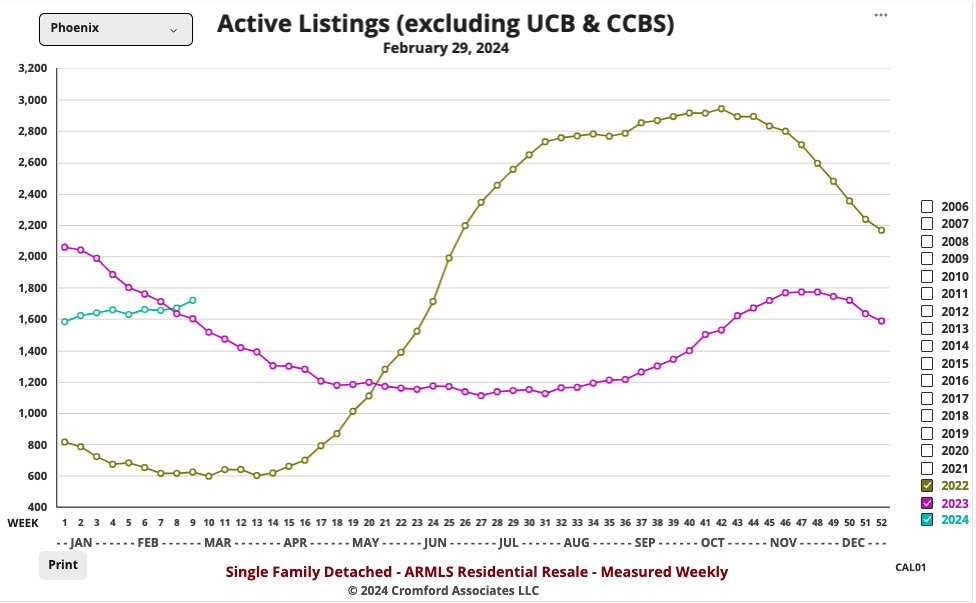

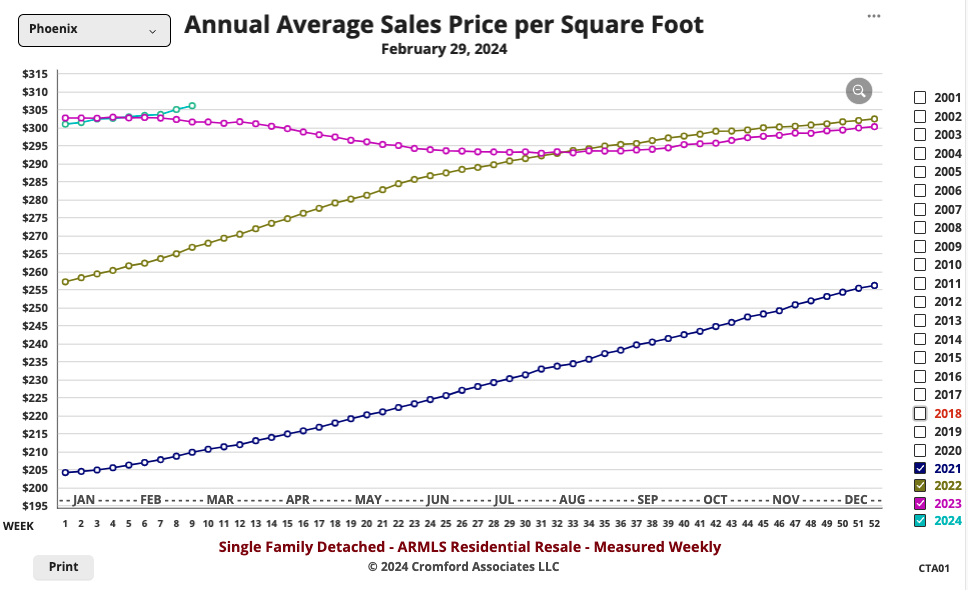

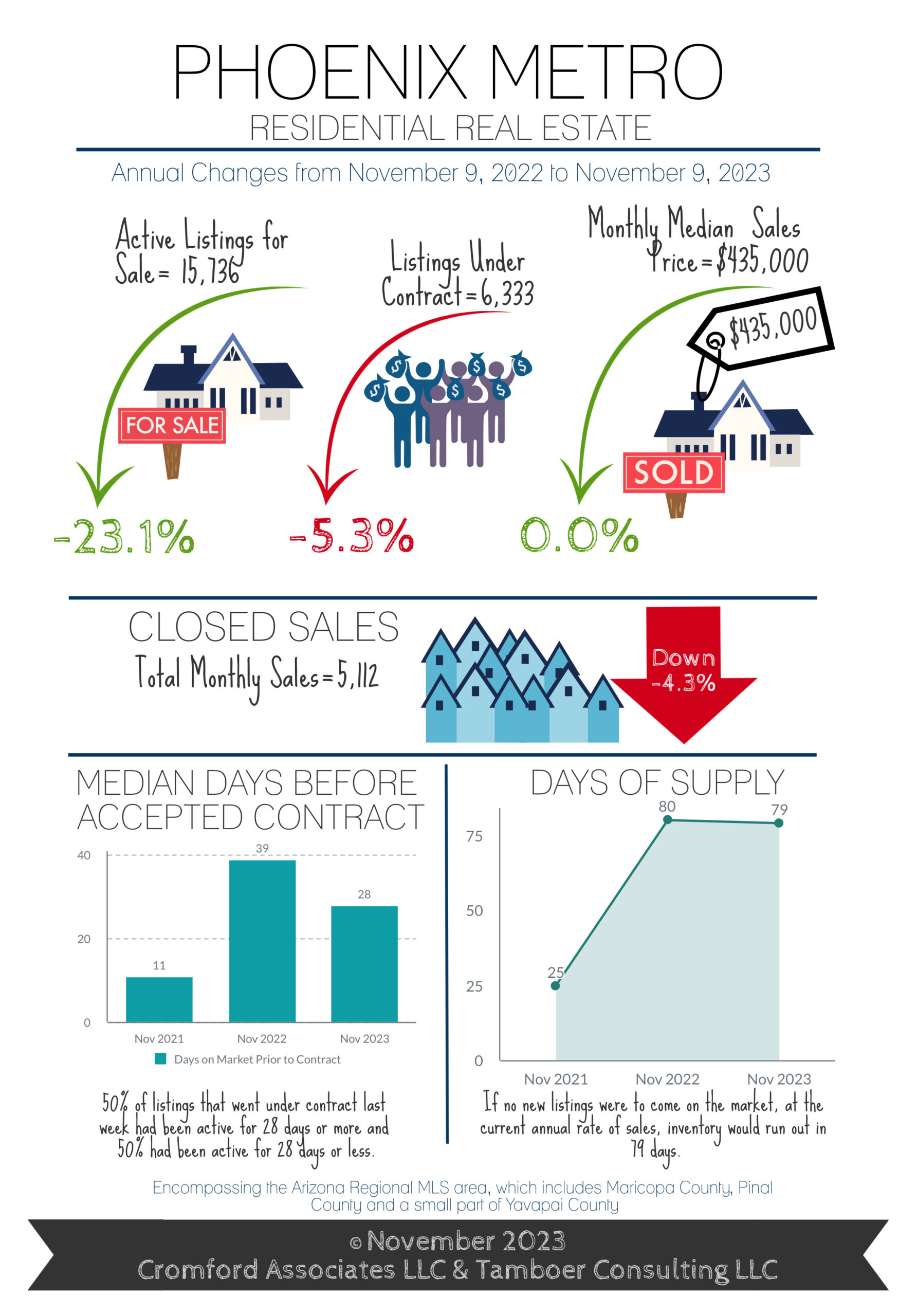

Here are the basics from The Cromford Report – “the ARMLS numbers for March 1, 2024 compared with March 1, 2023:

Active Listings: 16,568 versus 14,739 last year – up 12% – and up 6.4% from 15,574 last month

Monthly Sales: 5,720 versus 5,706 last year – up 0.2% – and up 29% from 4,435 last month

Monthly Average Sales Price per Sq. Ft.: $293.70 versus $271.11 last year – up 8.3% – and up 1.7% from $288.74 last month

This set of numbers is a little disappointing, but by no means disastrous. On the bright side, closed listing counts for February 2024 managed to exceed February 2023, but only by 0.2%. This is not the recovery in volume that so many are impatiently hoping for. Also brighter, sales pricing performed better than anticipated and was up 1.7% from last month based on the monthly average sales price per square foot. The monthly median sale price rose by $10,000 too. However the rate at which contracts are getting signatures is lower than we expected and much lower than normal. We are starting March with only 8,693 listings under contract, down 4.6% from this time last year. And last year was well below normal.

The slow contract signing rate means active listing counts have continued to grow steadily, up by 2,000 since the start of the year. Last year we saw a fall of over 1,500 over the same period, because new supply was much scarcer then. It was the decline in supply that allowed us to scoff a year ago when Goldman Sachs published their ludicrous forecast that Arizona home prices would fall to 2008 levels in 2023. That certainly proved they had no idea what they were talking about. Prices are now up 8.3% from this time last year.

There is still no sign of a market crash in the short or medium term, but the market is struggling to gain traction. The healthy amount of incoming supply is not quite matched by a small improvement in demand and the balance between sellers and buyers only favors sellers by a small amount when considering the market as a whole. In many sectors of the market, buyers have more negotiating room, even though, judging by the recent price movements, most of them do not seem to realize this.

by homes under $1 million still have a tight supply and buyers outnumber sellers in most of these areas.

Market conditions are currently quite stable, so the idea that some sort of collapse is imminent is extremely far-fetched. However conditions can and often do change with little notice, so it is always worth to keeping a close eye on the key numbers.”

Ready to take advantage of the mild winter we love here? I am. You’ll see me out and about. Here are some good reads and events for your consideration.

Tea Tours at the Japanese Friendship Garden. Japanese tea is seen as an inseparable part of Japanese Culture, with production and practices that started centuries ago. Over time, changes in tea traditions and practices have led to the creation of various schools of tea, cafes, and casual enjoyment, but the pervasiveness in the culture around tea continues to this day. In Japan, having tea allows guests to take a break from the outside world and focus on the simple, transitory moment of serving and drinking tea. $50. Multiple dates and times available.

Get Your Personal Electrification Planner. “Electrification” is the process of eliminating poisonous methane gas from your home and installing dramatically more efficient (and less polluting) electric appliances. I’m doing this in my home. I just got rid of my gas stove, which groups like the American Lung Association show increase risks of lung health issues for children and the elderly. My next step will be to get rid of my gas water heater and shut down dangerous methane gas service to my house completely. This handy website from Rewiring America will help you electrify your home, and save money in the process.

Ride a bike on a tight wire 15 feet in the air.No problem! Reopening after being closed for more than 3 years, you’re invited to experience the Evans Family Skycycle. Suspended nearly 15 feet in the air, the Evans Family SkyCycle teaches riders about the principles of counterbalance and center of gravity while riding the 90-foot cable. The exhibit price is $7. General admission tickets are required. Safety Restrictions Apply. Opportunities occur daily.

Plan ahead for the Local First Good Business Summit. If you are building your local business, you’ll want to be at this keynote Local First Arizona event. It’s an opportunity for locally-owned businesses from across the state to connect and grow as leaders in their communities — working together to form lasting relationships that create meaningful impact for a stronger, more resilient Arizona. It’s an opportunity to be seen, to be heard and to make a change.

Find a Local Business. While we are talking about local businesses, you may or may not know that a great way to support local businesses is to check the Local Business Directory before you shop. It’s easy to default to an out-of-state brand or franchise. This way you can support your community and retain more of your dollars in Arizona.

Jane Goodall Gives us a little hope. Jane Goodall – Reasons for Hope is an uplifting journey around the globe to highlight good news stories that inspire people to make a difference in the world around them. Featured stories such as the Northern Bald Ibis’ migration over the Alps, the re-introduction of the American Bison by the Blackfeet Nation, the worldwide recognized Sudbury Regreening Story, and inspiring youth-led initiatives involved in Jane Goodall’s Roots & Shoots align with historical footage of Jane’s beginnings as a chimpanzee researcher. Jane revolutionized how we view the world around us. Join her on this adventure of inspiration and hope. Irene P. Flinn Theatre. $9 plus general admission. Daily 11:00 AM & 1:00 PM.

Wellness Check List for 2024. I found this nice article that summarizes, and kinda serves as a checklist of ways to live in better balance. Personal health and general sustainability can go hand-in-hand, and this article is a nice summary. It’s given me a few ideas of things I’d like to try this year.

Free Spanish Classes at Barcoa. This is one of the most creative ideas I’ve seen in a while. Evidently patterned after the learn-then-try dance classes that you see all over town. After 90 minutes of learning about Mexican culture and how to speak the language, enjoy an all-night happy hour in the basement with 20% off all cocktails and flights. This is beginner-level Spanish and probably the only school in town where the bar is open! First come basis. Free. The question is how much can you learn after a couple happy hour drinks?

We are hearing from fellow agents that they are busy, but we know there is still a shortage in the market. Paradoxically, a shortage does make agents scramble.

The numbers from the Cromford Report are telling us that the recent interest rate news has not changed the situation much.

For Buyers Well the balanced market didn’t last long, 7 weeks to be exact. Last month the Federal Reserve gave the housing industry a much needed gift. Not only did they not raise the Federal Funds Rate, they also announced their intention to drop it three times in 2024. Conventional mortgage rates responded by dropping from 7.1% to 6.62% within 2 days. Mortgage rates have now dropped 1.4% since they peaked at 8% in October 2023, saving a borrower nearly $380 per month on a $400,000 loan, a payment decline of 13%. For perspective, each time the rate drops by 1%, the mortgage payment can drop between 9-10% depending on where it started, in many cases saving at least $200/month*. This rate drop was enough to give December’s mortgage applications a boost, which could be a precursor to January’s accepted contract counts.

So what can Greater Phoenix expect for 2024? It’s reasonable to expect some relief, not in the form of declining prices but in declining mortgage payments. Combine this with rising family incomes and we can expect affordability measures to improve along with demand. It’s not reasonable to expect another insane market with skyrocketing prices like 2020-2021, or another 12.5% drop in values like 2022. It could be quite boring in terms of price for the first quarter, but uplifting with more traditional home buyers getting back in the game. Things could get more exciting after the Federal Reserve meets again at the end of January and further reveals their plan for the Federal Funds rate in 2024. Stay tuned.

For Sellers While Greater Phoenix is out of a balanced market and continually improving, the seller’s market is still very weak so a combination of good condition and price remains key to facilitating an offer within a reasonable time frame, along with an open mind regarding concessions to the buyer. New listings so far in the first week of January are higher than last year, but not high, and while inventory is beginning to rise moderately it’s still 37% below normal for this time of year.

Not all cities are in a seller’s market, the distribution is as follows from strongest-to-weakest:

Seller’s Markets: Tolleson, Apache Junction, Fountain Hills, Chandler, Gilbert, Laveen, El Mirage, Anthem, Glendale, Sun Lakes, Phoenix, Scottsdale, Mesa, Avondale

Balanced Markets: Tempe, Litchfield Park, Sun City West, Peoria, Goodyear, Surprise, Paradise Valley, Arizona City

Buyer’s Markets: Cave Creek, Gold Canyon, Queen Creek, Sun City, Casa Grande, Buckeye, Maricopa

Most cities are either gradually improving or holding steady in their market measures. Sale price measures in January will reflect December negotiations, but with this turn in the market fueled by lower mortgage rates and seller concessions we can expect sales price measures to be sustained in the first quarter. The second quarter could get exciting if rates continue down.

*Talk to a qualified lender to determine your specific circumstance

I wanted to take a moment to thank all of the volunteers who made Phoestivus so great this year. In particular, I’d like to thank Samantha Davis Jackson, Lisa Banish, Sara Esther Anderson for their tireless work to make it happen. (This event takes thousands of hours to put together.)

Special props to Erica Shipione who pulled together an amazing media effort. We got more coverage than ever before.

Thank you to Brooks Werner for arranging Hipster Santa to join us once again. So many people were so excited to see him there.

Thank you, Walter Studios for organizing our first ever speakeasy. It was a hit!

The staff, volunteers and venders show up early on Friday to set up and are there late every night so our community can enjoy all the fun.

We took a couple major hits in recent years, with Covid and then being moved to a new location.

I’m happy to report that we have more than recovered. Our goal was to remind past attendees of the fun of this event and introduced Phoestivus to thousands more who are new to downtown.

There is a particular “Phoestivus Pheeling” that is so strong at Phoestivus. It is the feeling that this is our unique event, that we’ve all pitched in to make it what it is, and that we can feel a deeply shared joy that is absent from our consumption-driven holidays.

It is why this is the happiest time of the year for me.

That feeling was very strong this year and it inspires me to re-commit to this event for years to come.

In 2024 expect more vendors, more people and more quirky activities that set Phoestivus apart from other events. If you have ideas for fun features, please let me know!

As we go in to the new year there is cause for cautious optimism. Treasury Secretary Janet Yellen said last week that the economy has achieved the “soft landing” that they were hoping for with all of the interest rate increases.

While interest rates are still historically high, this optimism is an early signal that they could really start to drop in 2024.

If you are a regular reader, I’ve predicted that market conditions will begin to improve as soon as the Fed announces that they will not raise, or even reduce interest rates. According to the Cromford Report (below), we’ve not seen that yet. But, I’m not ready to concede. The holidays always run slower than other moths. I think we will see more buyer activity in 2024.

If you are thinking of selling, get ready. Buyers will see that, even if they come in with a high interest rate when they buy, all they will need is a drop of over 1% sometime in the next couple years for a refinance to pencil out. So, they will re-enter the market in 2024. Remember, there continues to be an influx of new residents, plus the institutional investors plus STRs continue to own almost 15% of the inventory. So, inventory will remain tight.

If you are thinking of buying, save your money aggressively and negotiate that raise so you will be ready. Don’t expect the crazy days of 2019-21, but watch for new listings to increase.

Turning to our friends at the Cromford Report, we see a December with fewer listings, and increasing prices.

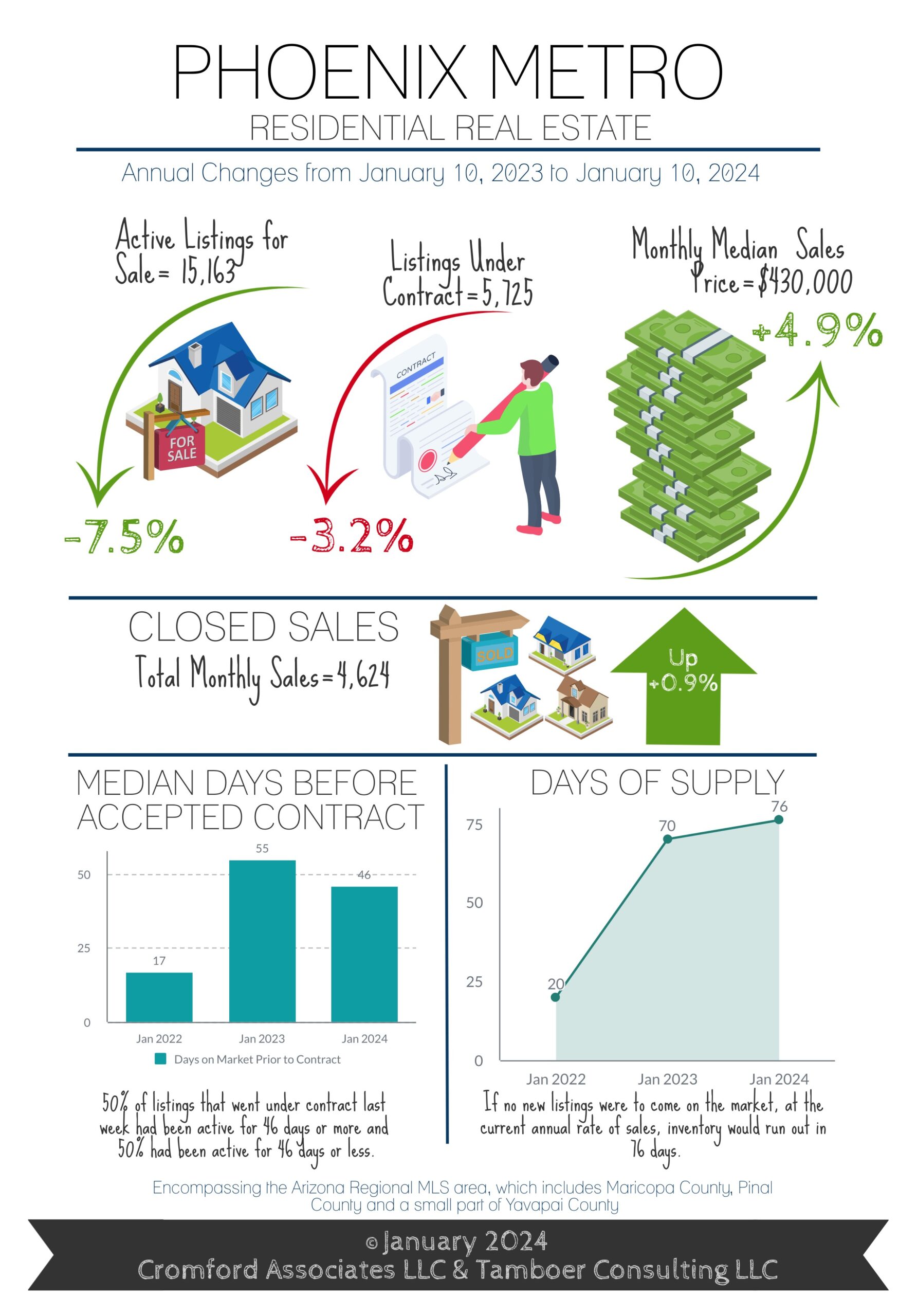

“Here are the basics – the ARMLS numbers for January 1, 2024 compared with January 1, 2023 for all areas & types:

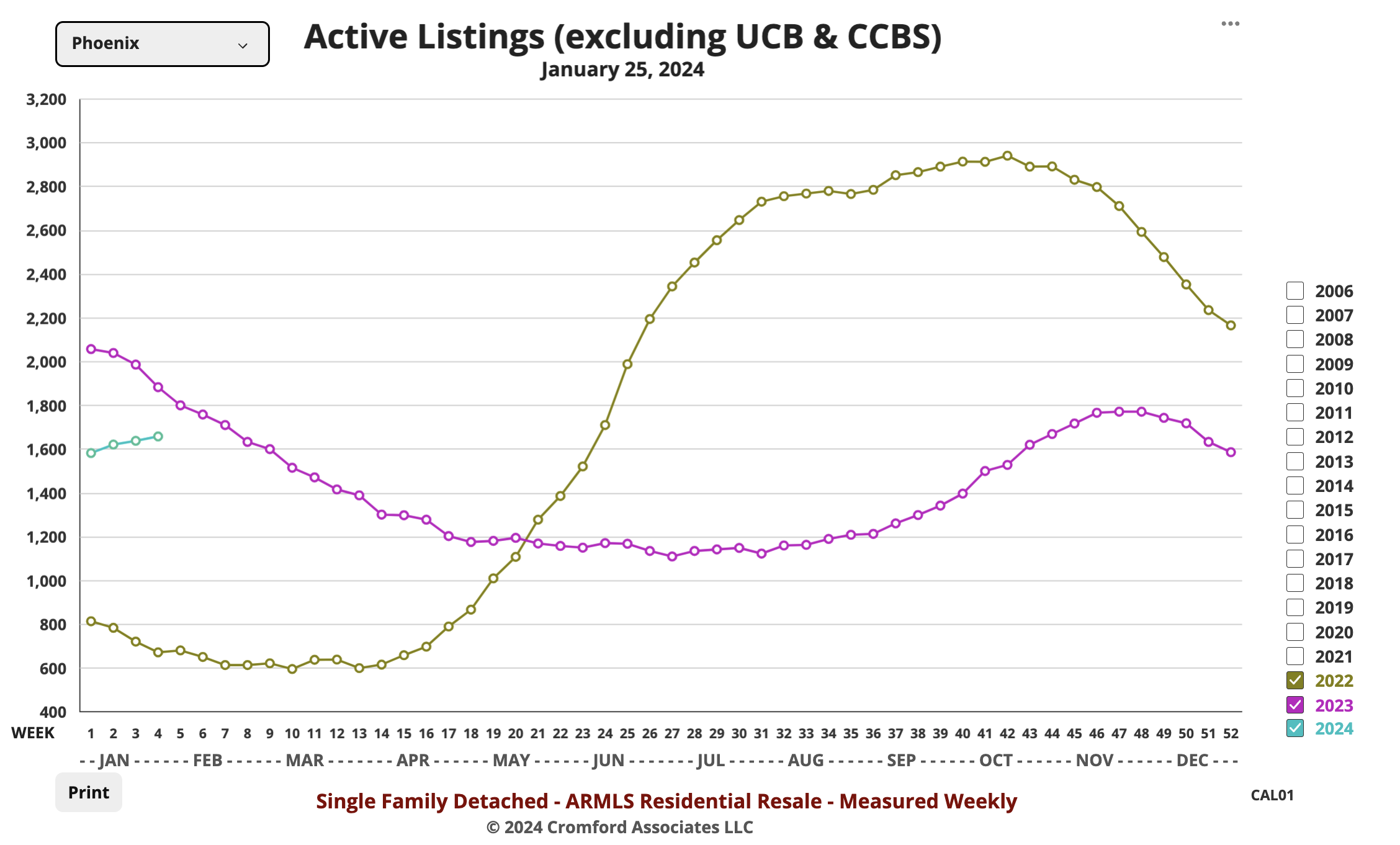

Active Listings (excluding UCB & CCBS): 14,593 versus 16,298 last year – down 10.5% – and down 8.7% from 15,981 last month

Pending Listings: 3,263 versus 3,657 last year – down 10.8% – and down 14.1% from 3,798 last month

Monthly Sales: 4,929 versus 5,138 last year – down 4.1% – but up 6.4% from 4,634 last month

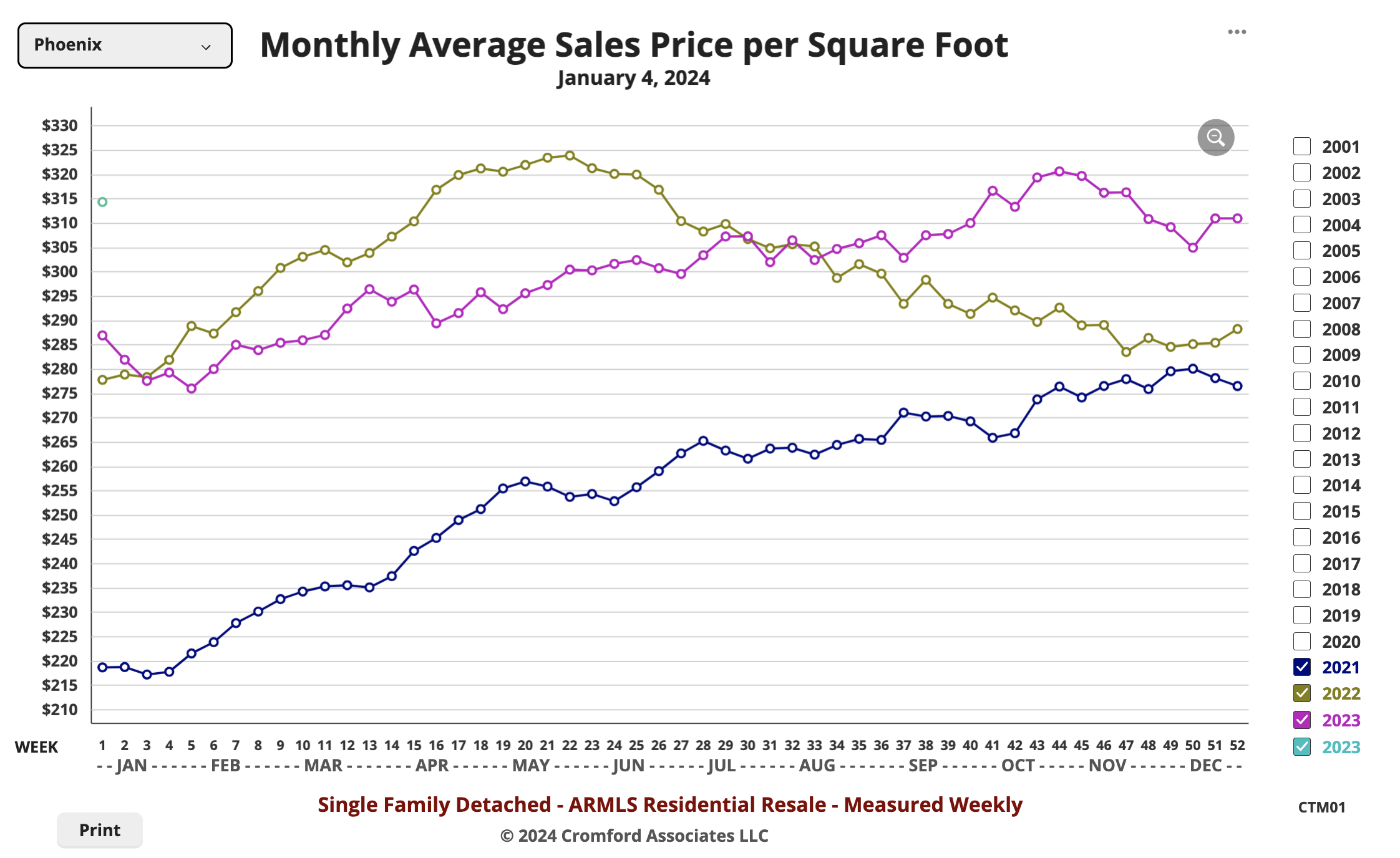

Monthly Average Sales Price per Sq. Ft.: $284.85 versus $265.90 last year – up 7.1% – but down 1.5% from $289.30 last month

The market has improved for sellers in some ways since last month. The supply of active listings is down almost 9% since December 1 and down more than 10% from a year ago. It is always good for a seller to have less competition from other homes. The monthly sales count for December was an improvement over November, but is still down from a year ago, when things were already not too good. So this is neutral for sellers. The pending and under contract counts are downright bad for sellers, down sharply from last month and significantly lower than a year ago.

Considering how much mortgage rates have fallen in the last two months, the numbers can be described as fairly disappointing from a seller’s perspective. Lower mortgage rates are supposed to bring out more buyers. So far that is barely noticeable. From a buyer’s perspective this is good news because they have less competition to worry about.

Prices are still stable, up by more than 7% from this time last year when measured by $/SF, and up 4.4% if measured by median sales price. This is a shade more than the latest rise in the Consumer Price Index. The difference between the two price measurements is caused by the strength in pricing in the luxury market. Median sales prices are dominated by the entry-level and mid-range markets which have been weaker than the top end.

We are still very short of 2024 data to show which way things are heading. Both supply and demand are picking up, as we would always expect in January. Supply has risen 0.5% in the first 3 days while listings under contract are up 3%. This is barely enough data to draw a conclusion, but the indicators are better for sellers than buyers. The contract ratio has risen from 35.13 to 35.98. This is consistent with a neutral, balanced market, but with the trend again moving in favor of sellers.

Expect slower activity around the holidays, but a boost in the near year as all those people who were put to sleep by turkey, or were busy hiding their elf on the shelf all December decide to get active again.

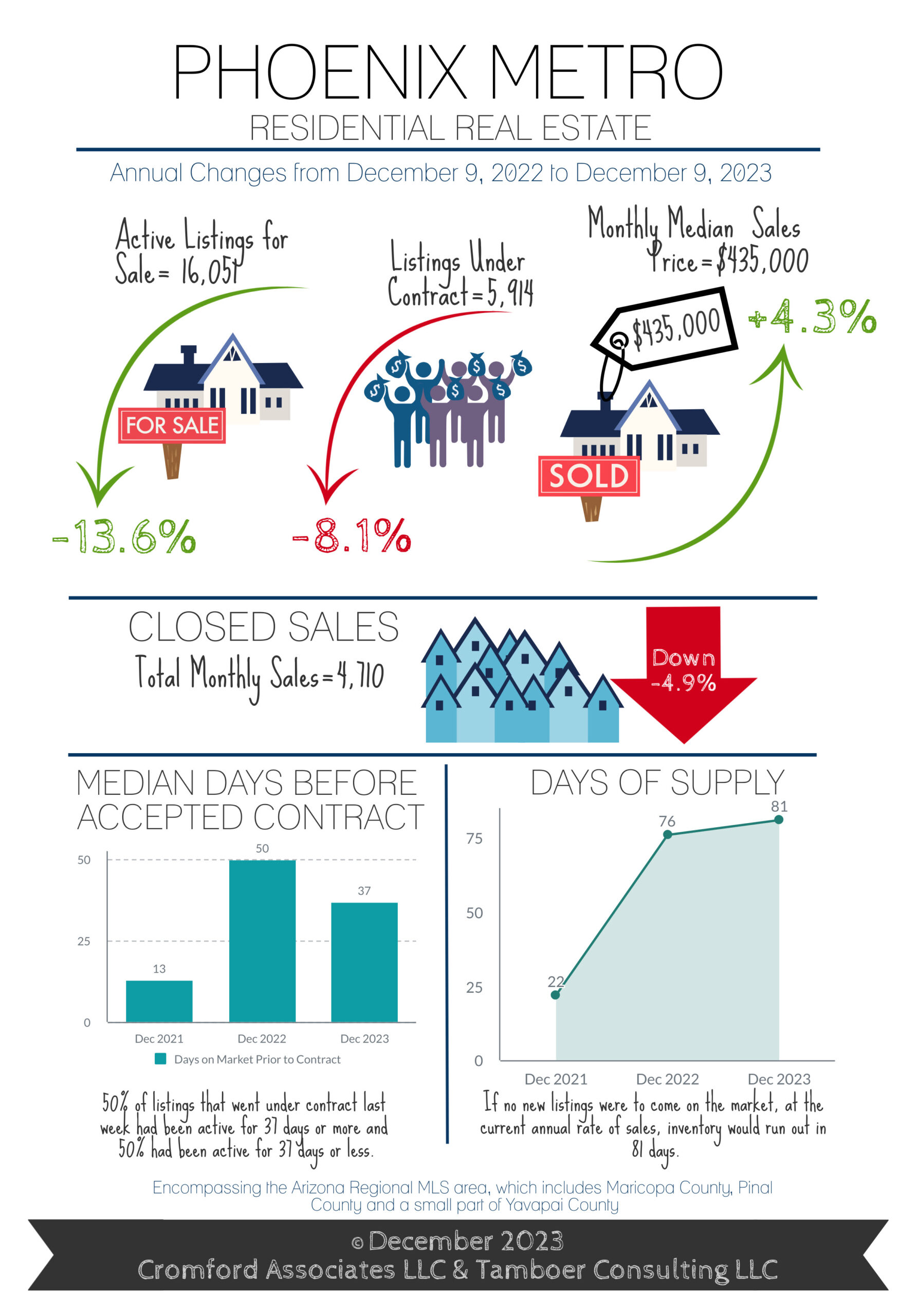

Here are the basics – the ARMLS numbers for December 1, 2023 compared with December 1, 2022 for all areas & types:

Active Listings (excluding UCB & CCBS): 15,981 versus 19,155 last year – down 17% – but up 4.8% from 15,247 last month

Active Listings (including UCB & CCBS): 18,050 versus 21,206 last year – down 15% – but up 4.0% compared with 17,364 last month

Pending Listings: 3,798 versus 4,301 last year – down 12% – and down 2.9% from 3,911 last month

Monthly Sales: 4,616 versus 4,928 last year – down 6.3% – and down 11% from 5,210 last month

Monthly Average Sales Price per Sq. Ft.: $288.97 versus $272.29 last year – up 6.1% – but down 2.1% from $295.13 last month

Monthly Median Sales Price: $439,000 versus $420,000 last year – up 4.6% – and up 0.9% from $435,000 last month

After rising during October, and peaking at an average just over 8% mid-month, mortgage rates declined thereafter and tumbled throughout November. In theory this should have injected some life into housing demand, but there is precious little evidence of this in the numbers above. We have fewer homes under contract than last month and far fewer than a year ago, when we were all depressed about the low demand. Sales counts are also down from last year and last month reaching the unusually low level of 4,616 in November.

One reason for the severe lack of demand may be that home prices are noticeably higher than a year ago, something few people were predicting 12 months ago. Over the last months there were mixed signals. The median sales price grew almost 1% but the average price per square foot dropped by over 2%. This followed a sharp in crease the month before. When this happens it is usually caused by the luxury market. With much lower unit volumes, the luxury market can vary a lot month to month and the effect on the $/SF can be substantial. The luxury market has negligible effect on the median sales price. The median sales price tends to be strongly influenced by unit volumes at the low end. Despite the weak demand, supply is still below normal which is preventing prices from tumbling. Supply has risen for several months but is now stable again as few people list there homes in December and several take their homes off the market for the holiday season. We anticipate more supply appearing in January.

The new home market continues to outperform the re-sale market. Mortgage rate buy-downs have kept new home demand at a healthy level.

December is not usually a month for us to see a flood of new home buyers, so we anticipate the the second half of January will tell us whether buyers see a big difference between mortgage rates around 7% compared with 8%. The last 12 months have been full of surprises, so caution and watching the statistics carefully is still the order of the day.

Co-op living is great if you need a space that is maintained like an apartment, but you want to own it. Its great if you don’t expect to be nearby all the time. It’s also great if you like a strong and secure community. The one thing to always remember is that co-ops are always cash only, since you are buying what amounts to a share in a corporate entity. Another thing to remember is that the HOA fees seem really high. However, they cover so much more than most HOAs, often including utilities and taxes.

The price of our listing in midtown has come down a bit and the sellers are very reasonable, though not in a rush. So, have a look.

520 W. Clarendon Ave, Unit G2. $286,000, 2br/1.75 ba, 1,320sf. There are a few pristine co-op apartments still in central and downtown Phoenix. Most were built in the 1960s and only a few maintain that mid-century charm. This is one of them. But, on top of that, the owners of this unit opened up the kitchen since and completely remodeled since they purchased the home in 2021. This home is being sold with all of the unique furniture, as an option for the buyer. This secure community is just steps from dining, light rail and shopping. You can lounge in the pool or chill in the historic commons knowing that your investment is being maintained and cared for as a co-op uniquely is. See the listing and more photos here.

No lie, 2020 did a number on Phoestivus. Attendance dropped when we came back in 2021.

Then some faceless developer took our old spot at Central and McKinley to build yet another apartment building with ground floor space full, not of local shops, but with treadmills and exercise equipment.

Do I sound bitter?

Well, about the multitude of community-killing apartments, yes. But not about Phoestivus.

On that I’m bullish.

Despite the setbacks, we grew stronger and we survived. Phoestivus is back and bigger than ever. It now runs Thursday, Friday and Saturday morning, December 14th – 16th.

It is getting more and more like the old German Christmas markets of my youth, which partially inspired Phoestivus back in 2010.

We have an opportunity this year to remind folks why they came, but also to introduce Phoestivus to the thousands of people who have moved in to downtown since we were at the old location.

I’m excited to say that the original Hipster Santa is back!

If you know, you know. And if you know, you are excited by the news.

In addition, we have many of the favorites. We have the Pheats of Strength, the Phoestivus Pole, the Airing of Grievances, food trucks, local beers, and of course over 150 vendors.

Share a ride because parking might be a challenge.