November Market Update

In this November Market Update, we are continuing to monitor a dramatically lower number of listing as compared to this time in 2019. This data comes to you from The Cromford Report and covers all areas and all types of homes.

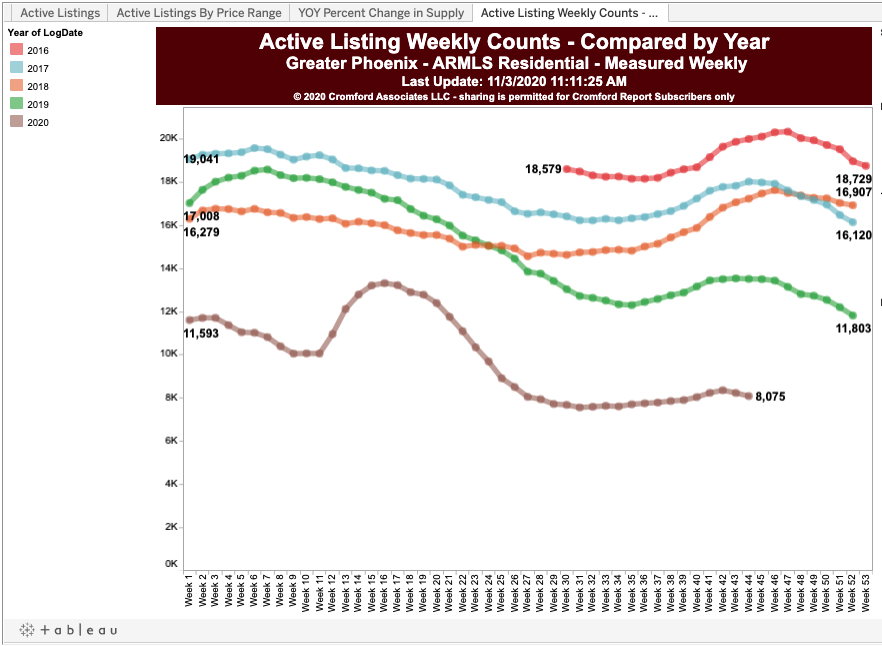

- Active Listings (excluding UCB & CCBS): 8,682 versus 14,525 last year – down 40.2% – but up 7.4% from 8,101 last month

- Active Listings (including UCB & CCBS): 13,901 versus 18,322 last year – down 24.1% – but up 4.5% compared with 13,305 last month

- Pending Listings: 7,862 versus 5,919 last year – up 32.8% – but down 1.7% from 7,999 last month

- Under Contract Listings (including Pending, CCBS & UCB): 13,081 versus 9,716 last year – up 34.6% – but down 0.9% from 13,203 last month

- Monthly Sales: 9,992 versus 8,037 last year – up 20.5% – and up 3.6% from 9,641 last month

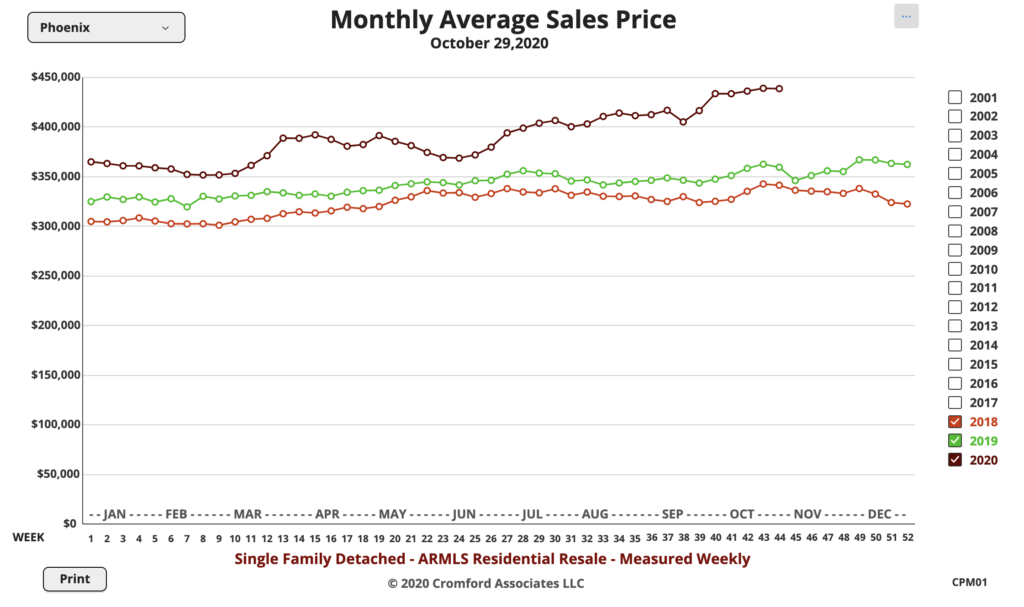

- Monthly Average Sales Price per Sq. Ft.: $207.37 versus $174.14 last year – up 19.1% – and up 4.3% from $198.84 last month

- Monthly Median Sales Price: $332,000 versus $285,000 last year – up 16.5% – and up 1.6% from $326,800 last month

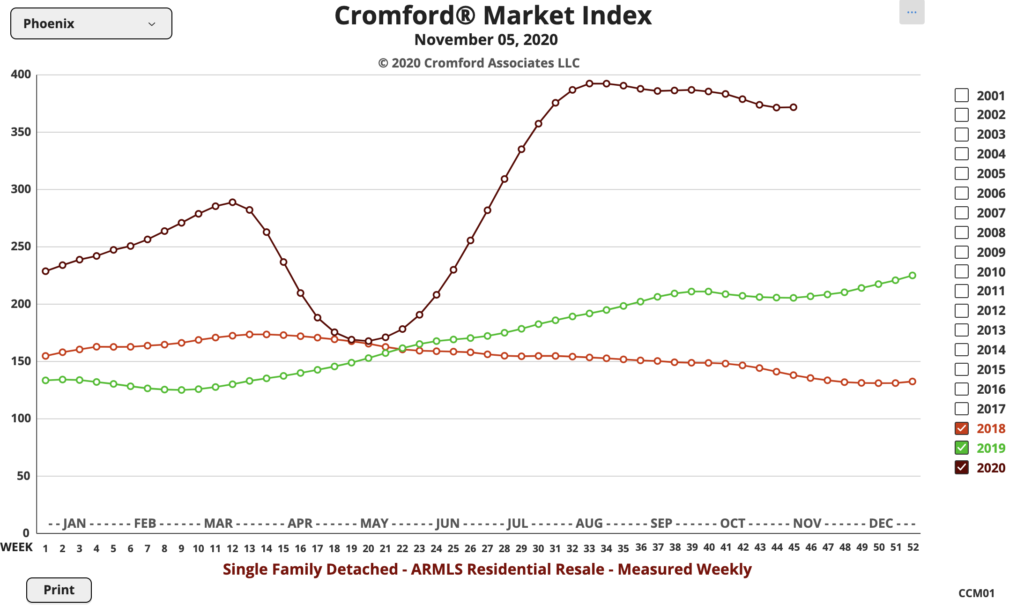

The flow of new listings remained strong until late October but has started to fade noticeably over the last weeks. Since we are already very short of supply, this does not bode well for buyers who are likely to be fighting each other over a dwindling list of homes for sale during the last 2 months of the year. With demand at a very high level, especially for the normally quiet fourth quarter, the market is even more out of balance than it was last month.

Closed sales were over 20% higher than in 2019 during October. This is even more remarkable given that in 2019 October had 23 working days, 1 more than in 2020. With the average price per square foot up over 19% from last year, the dollar volume is exceptionally high at $4,272 million, up from $2,786 million last year. And last year we thought we had a strong market. We are running out of superlatives to describe the state of the current market.

Average and median prices are running away skywards, but some of this is fueled by a sales mix which increasingly favors upscale properties. During October we saw 37 closed listings over $3 million. This is not only the highest total for any October in history, it is the highest total for any month in history. The average for all months since 2001 is 9 and in October 2019 we counted 10.

The size of the market below $300,000 is shrinking fast, constrained by lack of supply and by the fact that last year’s home at $270,000 is now priced well over $300,000. However any home priced under $300,000 is likely to see hordes of buyers.

Is there any sign of the upward surge in pricing losing pace as we enter the November market? In a word – No.

At this time last year we had no idea of the impending pandemic, but unless something similarly surprising happens in the next few months, the housing market in Greater Phoenix is unlikely to stop rising.

We can help you build a strategy to buy or sell a home, even in this crazy market. We have the experience to help guide you. Call us at 602-456-9388.