February Market Look-Ahead

We are hearing from fellow agents that they are busy, but we know there is still a shortage in the market. Paradoxically, a shortage does make agents scramble.

The numbers from the Cromford Report are telling us that the recent interest rate news has not changed the situation much.

For Buyers

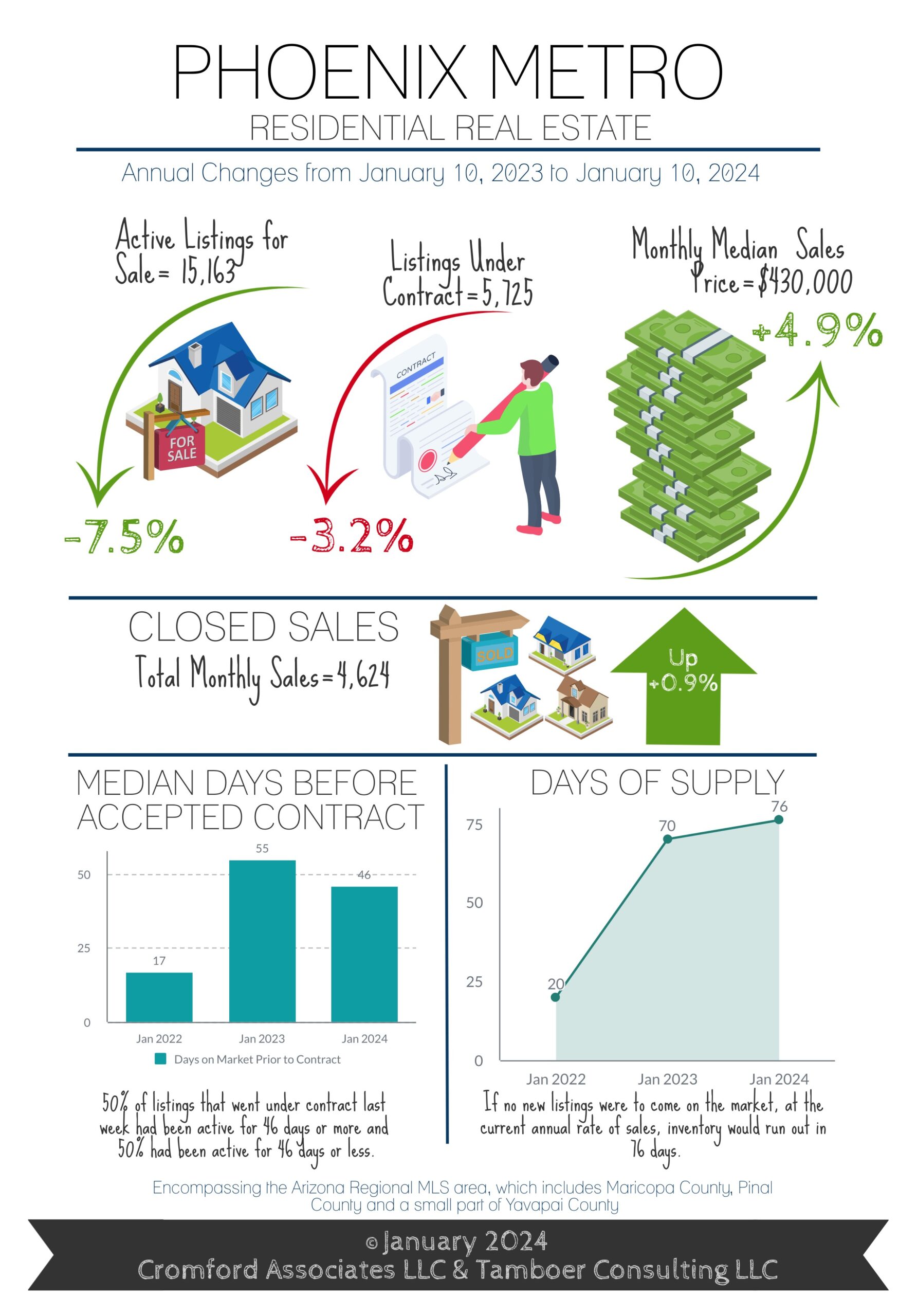

Well the balanced market didn’t last long, 7 weeks to be exact. Last month the Federal Reserve gave the housing industry a much needed gift. Not only did they not raise the Federal Funds Rate, they also announced their intention to drop it three times in 2024. Conventional mortgage rates responded by dropping from 7.1% to 6.62% within 2 days. Mortgage rates have now dropped 1.4% since they peaked at 8% in October 2023, saving a borrower nearly $380 per month on a $400,000 loan, a payment decline of 13%. For perspective, each time the rate drops by 1%, the mortgage payment can drop between 9-10% depending on where it started, in many cases saving at least $200/month*. This rate drop was enough to give December’s mortgage applications a boost, which could be a precursor to January’s accepted contract counts.

So what can Greater Phoenix expect for 2024? It’s reasonable to expect some relief, not in the form of declining prices but in declining mortgage payments. Combine this with rising family incomes and we can expect affordability measures to improve along with demand. It’s not reasonable to expect another insane market with skyrocketing prices like 2020-2021, or another 12.5% drop in values like 2022. It could be quite boring in terms of price for the first quarter, but uplifting with more traditional home buyers getting back in the game. Things could get more exciting after the Federal Reserve meets again at the end of January and further reveals their plan for the Federal Funds rate in 2024. Stay tuned.

For Sellers

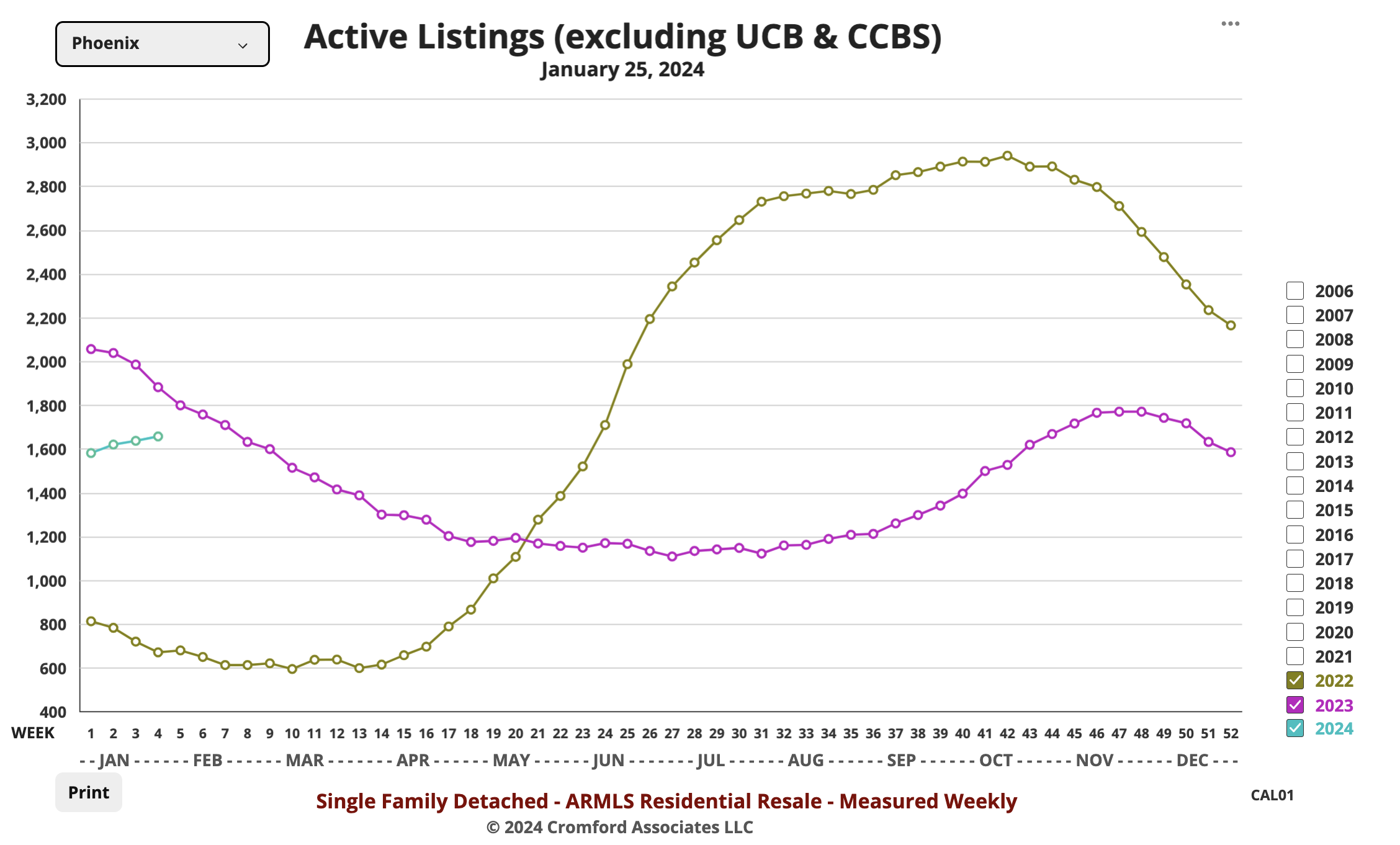

While Greater Phoenix is out of a balanced market and continually improving, the seller’s market is still very weak so a combination of good condition and price remains key to facilitating an offer within a reasonable time frame, along with an open mind regarding concessions to the buyer. New listings so far in the first week of January are higher than last year, but not high, and while inventory is beginning to rise moderately it’s still 37% below normal for this time of year.

Not all cities are in a seller’s market, the distribution is as follows from strongest-to-weakest:

Seller’s Markets: Tolleson, Apache Junction, Fountain Hills, Chandler, Gilbert, Laveen, El Mirage, Anthem, Glendale, Sun Lakes, Phoenix, Scottsdale, Mesa, Avondale

Balanced Markets: Tempe, Litchfield Park, Sun City West, Peoria, Goodyear, Surprise, Paradise Valley, Arizona City

Buyer’s Markets: Cave Creek, Gold Canyon, Queen Creek, Sun City, Casa Grande, Buckeye, Maricopa

Most cities are either gradually improving or holding steady in their market measures. Sale price measures in January will reflect December negotiations, but with this turn in the market fueled by lower mortgage rates and seller concessions we can expect sales price measures to be sustained in the first quarter. The second quarter could get exciting if rates continue down.

*Talk to a qualified lender to determine your specific circumstance