I wanted to take a moment to thank all of the volunteers who made Phoestivus so great this year. In particular, I’d like to thank Samantha Davis Jackson, Lisa Banish, Sara Esther Anderson for their tireless work to make it happen. (This event takes thousands of hours to put together.)

Special props to Erica Shipione who pulled together an amazing media effort. We got more coverage than ever before.

Thank you to Brooks Werner for arranging Hipster Santa to join us once again. So many people were so excited to see him there.

Thank you, Walter Studios for organizing our first ever speakeasy. It was a hit!

The staff, volunteers and venders show up early on Friday to set up and are there late every night so our community can enjoy all the fun.

We took a couple major hits in recent years, with Covid and then being moved to a new location.

I’m happy to report that we have more than recovered. Our goal was to remind past attendees of the fun of this event and introduced Phoestivus to thousands more who are new to downtown.

There is a particular “Phoestivus Pheeling” that is so strong at Phoestivus. It is the feeling that this is our unique event, that we’ve all pitched in to make it what it is, and that we can feel a deeply shared joy that is absent from our consumption-driven holidays.

It is why this is the happiest time of the year for me.

That feeling was very strong this year and it inspires me to re-commit to this event for years to come.

In 2024 expect more vendors, more people and more quirky activities that set Phoestivus apart from other events. If you have ideas for fun features, please let me know!

As we go in to the new year there is cause for cautious optimism. Treasury Secretary Janet Yellen said last week that the economy has achieved the “soft landing” that they were hoping for with all of the interest rate increases.

While interest rates are still historically high, this optimism is an early signal that they could really start to drop in 2024.

If you are a regular reader, I’ve predicted that market conditions will begin to improve as soon as the Fed announces that they will not raise, or even reduce interest rates. According to the Cromford Report (below), we’ve not seen that yet. But, I’m not ready to concede. The holidays always run slower than other moths. I think we will see more buyer activity in 2024.

If you are thinking of selling, get ready. Buyers will see that, even if they come in with a high interest rate when they buy, all they will need is a drop of over 1% sometime in the next couple years for a refinance to pencil out. So, they will re-enter the market in 2024. Remember, there continues to be an influx of new residents, plus the institutional investors plus STRs continue to own almost 15% of the inventory. So, inventory will remain tight.

If you are thinking of buying, save your money aggressively and negotiate that raise so you will be ready. Don’t expect the crazy days of 2019-21, but watch for new listings to increase.

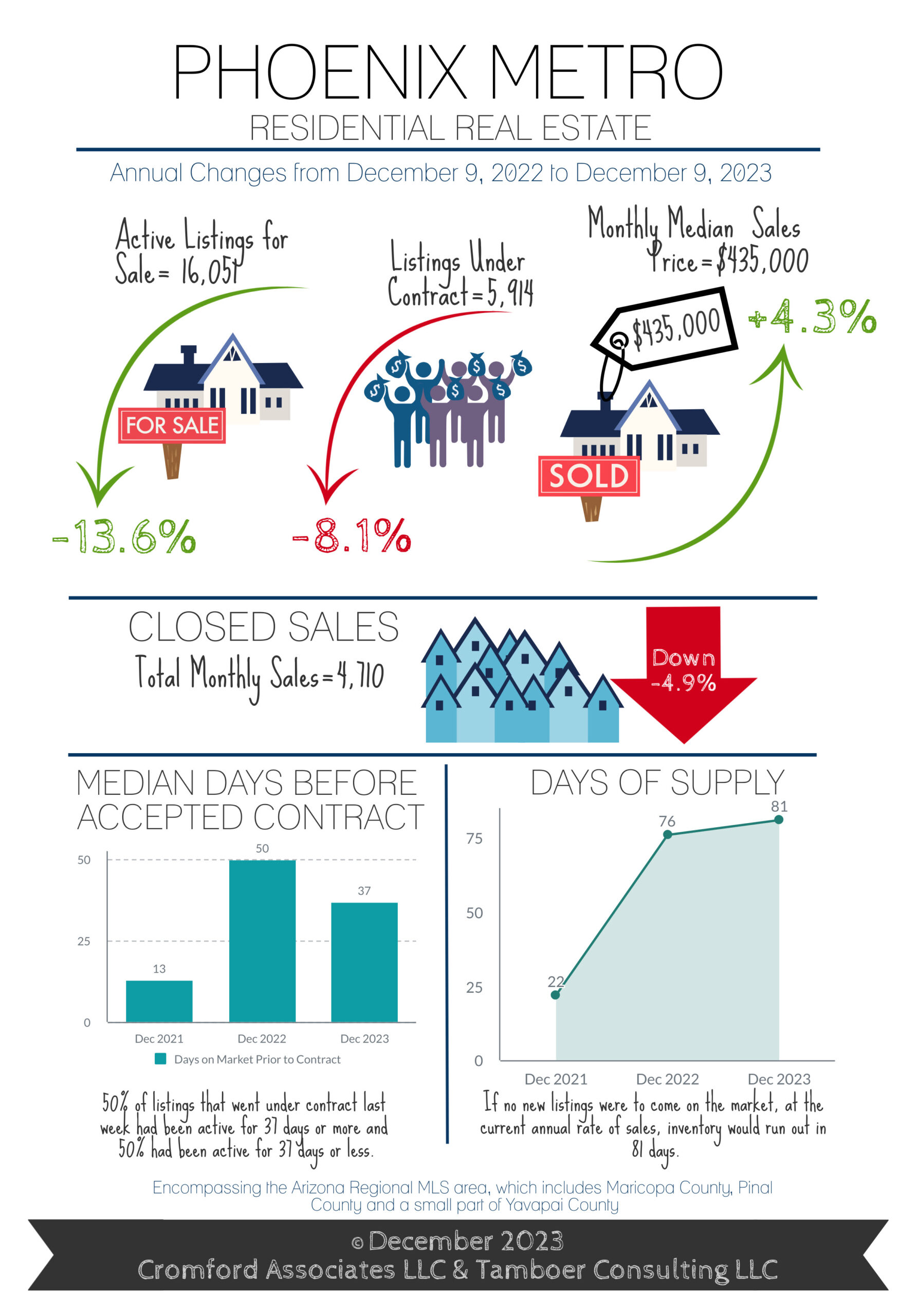

Turning to our friends at the Cromford Report, we see a December with fewer listings, and increasing prices.

“Here are the basics – the ARMLS numbers for January 1, 2024 compared with January 1, 2023 for all areas & types:

Active Listings (excluding UCB & CCBS): 14,593 versus 16,298 last year – down 10.5% – and down 8.7% from 15,981 last month

Pending Listings: 3,263 versus 3,657 last year – down 10.8% – and down 14.1% from 3,798 last month

Monthly Sales: 4,929 versus 5,138 last year – down 4.1% – but up 6.4% from 4,634 last month

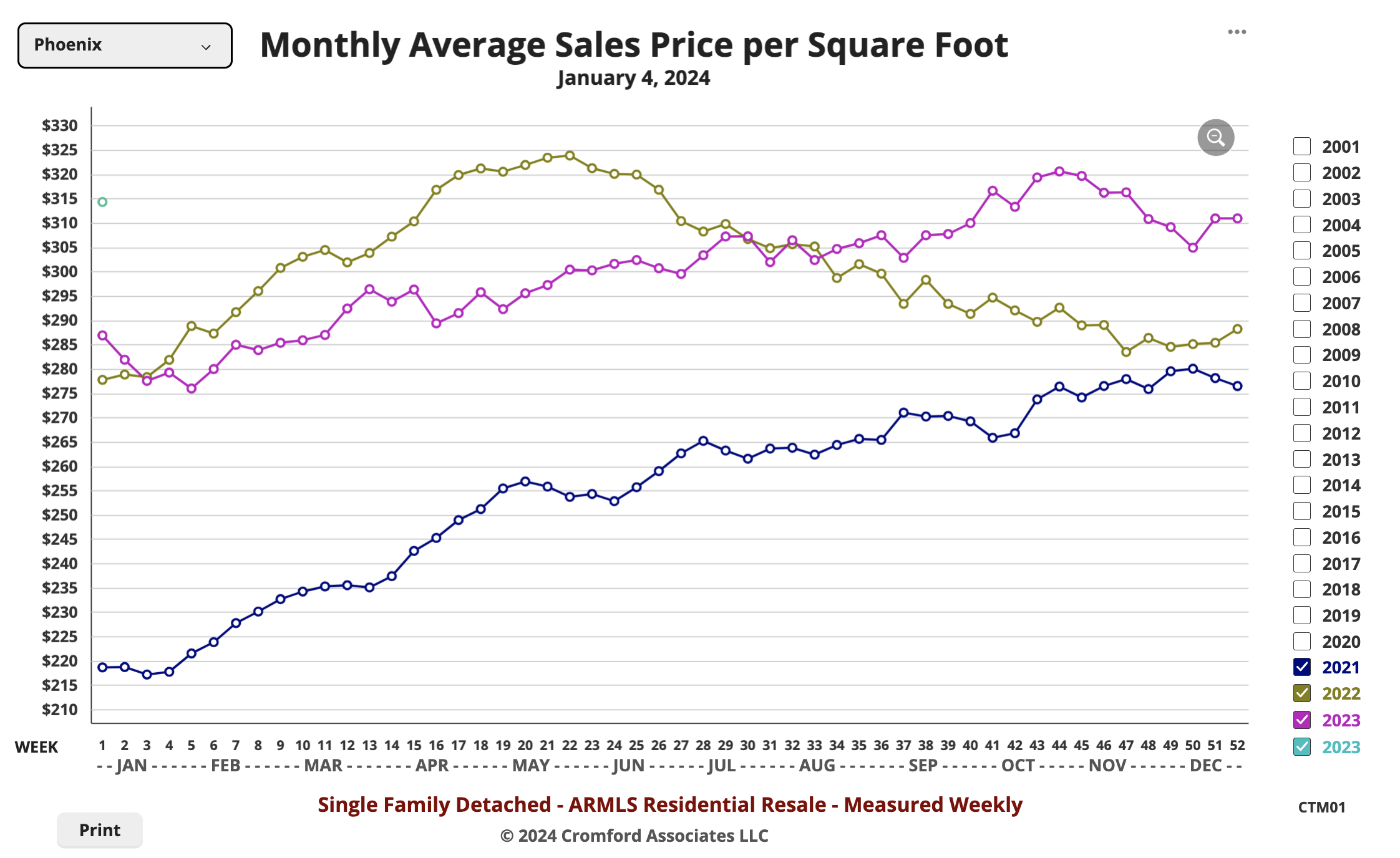

Monthly Average Sales Price per Sq. Ft.: $284.85 versus $265.90 last year – up 7.1% – but down 1.5% from $289.30 last month

The market has improved for sellers in some ways since last month. The supply of active listings is down almost 9% since December 1 and down more than 10% from a year ago. It is always good for a seller to have less competition from other homes. The monthly sales count for December was an improvement over November, but is still down from a year ago, when things were already not too good. So this is neutral for sellers. The pending and under contract counts are downright bad for sellers, down sharply from last month and significantly lower than a year ago.

Considering how much mortgage rates have fallen in the last two months, the numbers can be described as fairly disappointing from a seller’s perspective. Lower mortgage rates are supposed to bring out more buyers. So far that is barely noticeable. From a buyer’s perspective this is good news because they have less competition to worry about.

Prices are still stable, up by more than 7% from this time last year when measured by $/SF, and up 4.4% if measured by median sales price. This is a shade more than the latest rise in the Consumer Price Index. The difference between the two price measurements is caused by the strength in pricing in the luxury market. Median sales prices are dominated by the entry-level and mid-range markets which have been weaker than the top end.

We are still very short of 2024 data to show which way things are heading. Both supply and demand are picking up, as we would always expect in January. Supply has risen 0.5% in the first 3 days while listings under contract are up 3%. This is barely enough data to draw a conclusion, but the indicators are better for sellers than buyers. The contract ratio has risen from 35.13 to 35.98. This is consistent with a neutral, balanced market, but with the trend again moving in favor of sellers.